The inheritance tax (IHT) landscape is undergoing its most profound transformation in decades. To help professional advisers make sense of these changes, we partnered with Zurich UK for a Personal Finance Society (PFS) webinar exploring how recent and upcoming reforms are expanding the IHT net and reshaping client planning needs.

Hosted by Phil Day (Senior Business Development Manager, Iress), Michael France (Associate Product Manager, Iress), and Andy Roberts (Head of Specialist Protection, Zurich UK), the session explored how legislative change is bringing more clients into the IHT net, and how advisers can use cashflow modelling tools and protection sourcing technology to bring clarity to increasingly complex planning scenarios.

If you missed the live broadcast, you can watch the full CPD-accredited session here.

UK inheritance tax (IHT) changes: Why the net is tightening faster than ever

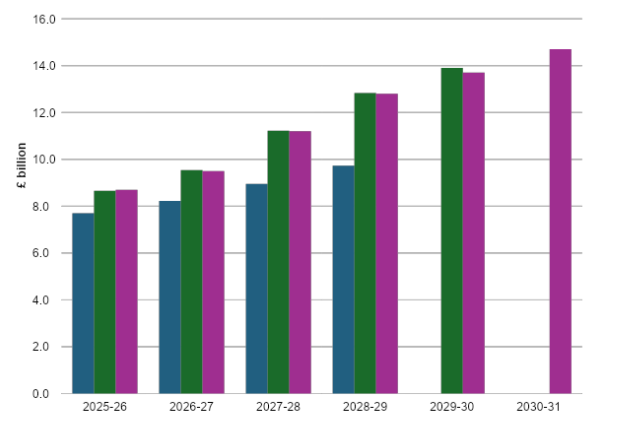

Inheritance tax can no longer be dismissed as a "voluntary levy" that’s easily avoided through basic planning. According to the Office for Budget Responsibility (OBR) March 2026 forecasts, annual IHT receipts are on track to climb exponentially, reaching an unprecedented £14.7 billion by 2031.

A combination of fiscal drag and aggressive structural legislative reforms is driving this surge:

- Frozen thresholds extended: The standard nil-rate bands have been frozen since 2008/09 and will remain capped until at least 2031, dragging ordinary families into scope via inflation.

- Residency-based regime: Effective 6 April 2025, the traditional domicile taxation framework was completely replaced by a residency-based regime.

- The tapering threshold trap: Both business/agricultural assets and inherited pensions will now count towards the £2 million Residence Nil-Rate Band (RNRB) taper threshold, accelerating the loss of allowances for affluent clients.

IHT receipts are forecast to reach £14.7bn by 2031

Source: OBR Economic and Fiscal Outlook - March 2024, October 2024, March 2026

How APR, BPR and AIM share reliefs have changed from April 2026

The rules governing Agricultural Property Relief (APR) and Business Property Relief (BPR) changed fundamentally on 6 April 2026. Advisers must carefully review any legacy arrangements relying on these allowances.

| APR, BPR and AIM reforms explained: Key legislative changes breakdown | ||

|---|---|---|

| Asset / relief type | Previous position | Position since 6 April 2026 |

| Combined APR & BPR qualifying assets | 100% relief from IHT after a standard 2-year holding period. | 100% relief is strictly capped at a combined £2.5 million per person; 50% relief applies to any value thereafter. (Note: The £2.5m allowance is transferable between spouses/civil partners.) |

| Alternative Investment Market (AIM) shares | Qualified for 100% BPR after being held for 2 years. | Restricted to 50% relief across the board, completely regardless of asset value. They do not qualify for the £2.5 million 100% allowance cap. |

Why pensions will fall inside the IHT net from April 2027

Perhaps the most significant disruption hits on 6 April 2027, when inherited pensions will officially come into scope for IHT. While death-in-service benefits and dependents' pensions are excluded, defined contribution (DC) and defined benefit (DB) schemes will face the full force of the tax.

The government estimates this change alone will impact 49,000 estates annually:

- 10,500 estates will face an entirely new IHT liability where they previously had none.

- 38,500 estates will see their existing IHT bills increase significantly.

What the 50% pension withholding rule means in practice (and its limitations)

The government subsequently announced a mechanism allowing pension scheme administrators to withhold 50% of a pension's value to pay the IHT directly. However, Andy Roberts highlighted critical drawbacks to this approach during the webinar.

It only pays the tax arising on the pension itself, does not solve the wider estate's liquidity issues, and faces major bottlenecks if the pension holds illiquid assets like commercial property or unquoted shares, which can take months or years to liquidate while late-payment interest compounds.

Turning IHT liabilities into effective protection strategies for clients

Identifying a liability is only half the battle; advisers need structural mechanisms to solve liquidity gaps before probate. The panel mapped out several real-world application frameworks:

- Matching protection to permanent vs temporary IHT shortfalls: For static liabilities, a Whole of Life (WOL) policy on a joint life second death (JLSD) basis remains the gold standard. For clients planning to downsize or gift assets aggressively, a Term to Age 90 policy can offer a drastically cheaper, tailored alternative to cover a temporary exposure window.

- Using gifting strategies and Inter Vivos policies to manage PET risk: To handle Potentially Exempt Transfer (PET) clawback risks, advisers can leverage multi-policy Gift Inter Vivos (GIV) frameworks. Sourcing whole-of-market quotes via Multi-benefit tools allows advisers to orchestrate 5 distinct term policies that perfectly mirror the 20% annual taper reduction seen between years 3 and 7.

- Using surplus income and NEOI rules to fund tax-efficient life cover: Instead of leaving unused pensions to be heavily taxed at death, retired clients with surplus income can systematically draw down from their pension via annuities or regular drawdowns to fund a life insurance policy written under trust. If properly structured, these premiums are classified as Normal Expenditure Out of Income (NEOI), meaning they are immediately exempt transfers that lower the taxable estate during the client’s lifetime.

How advisers can use technology to help clients understand evolving IHT planning needs

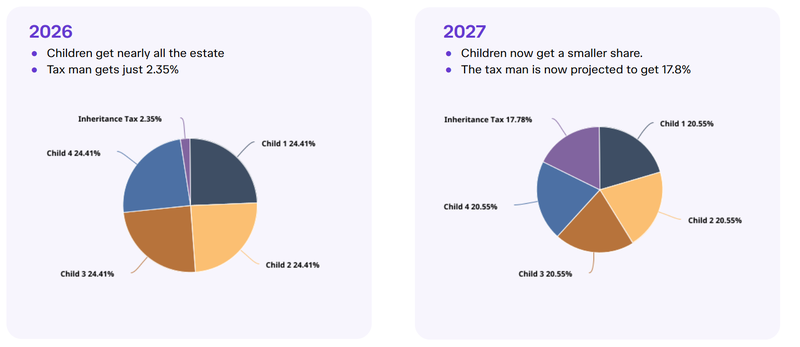

A central takeaway from the session was that IHT planning is no longer a static, one-time retirement event. Liabilities fluctuate dynamically as financial assets are depleted and illiquid property values continue to scale upward over time.

Visualising inheritance tax exposure over time

Using Xtools, the cash flow modelling software within Xplan, Michael France demonstrated how visually mapping this shifting asset mix can completely transform client engagement.

Instead of overwhelming a client with text-heavy legislation updates, you can instantly generate clear, interactive graphs that chart their gross wealth accumulation alongside their growing tax exposure over time. Showing a retired couple a visual breakdown of how the "taxman" is on track to overtake their children as the single largest beneficiary of their estate - sometimes scaling past 25% over a 30-year horizon - provides an undeniably compelling reason to act.

From cash flow insights to protection sourcing

Identifying a future shortfall is only step one. Phil Day demonstrated live how straightforward it is to future-proof a client's plan using The Exchange:

- Whole-of-Market comparisons in seconds: Rather than manually visiting individual provider portals, you can instantly run a whole-of-life or fixed-term quote on a Joint Life Second Death (JLSD) basis across the entire market simultaneously.

- Handling complex Tapered Liabilities: Using the built-in Multi-Benefit service on The Exchange, advisers can quickly construct the five separate level term policies needed to perfectly replicate a tailored Gift Inter Vivos framework to cover PET exposures.

- The premium gap reality check: The live demo illustrated that pricing a comprehensive £450,000 policy from day one is significantly more cost-effective for a client than waiting five years and setting up a secondary top-up policy. Sourcing early locks in the premium based on standard rates while the clients are younger and healthier, eliminating the risk of future medical exclusions or premium loading.

When you hook visual cashflow insights like those from Xtools directly into the instant sourcing capabilities of The Exchange, you give clients complete certainty. You aren't just selling a policy; you are visually proving its lifelong return on investment (ROI).

Bringing clarity to a fast-changing IHT landscape

As inheritance tax continues to evolve, advisers are facing a planning environment that is more complex, more dynamic, and more consequential for clients than ever before.

What this session made clear is that successful IHT planning is no longer about reacting to individual rule changes in isolation. It requires a joined-up approach that combines forward-looking cashflow modelling, a deep understanding of legislative shifts, and the ability to translate insight into actionable protection strategies.

By connecting technology like Xtools in Xplan with sourcing capabilities on The Exchange, advisers can move seamlessly from identifying future tax exposure to implementing tailored solutions that address both liquidity and legacy planning needs.

Ultimately, the goal is not just to highlight the size of the potential liability, but to give clients clarity, confidence and control over how their estate will be passed on.

Watch the webinar

The Demystifying the IHT shift webinar is now available on demand and is CPD-accredited.

In just three steps, learn how to:

- Unlock immediate cash to clear the probate hurdle

- Protect estate value from unnecessary tax erosion

- Build a flexible, long-term wealth roadmap

We also explore how interactive wealth modelling and modern protection sourcing can help turn complex conversations into clear, confident client outcomes.

This webinar is suitable for any adviser looking to strengthen their IHT conversations ahead of the 2026/2027 reforms.